Business Essentials – Employing People

What are my responsibilities as an employer?

As an employer in the UK, you have a number of legal and ethical responsibilities to ensure a safe, fair, and legally compliant working environment for your employees. These responsibilities span various areas, such as employment rights, health and safety, pay and tax obligations, and knowing who your employees are. You are likely to need the support of specialists as there are some complex issues to deal with in this area, and the legal responsibilities of employers are far reaching and ever changing.

Who needs to be paid via payroll? Who is an employee?

Self-employed individuals are not considered employees, so they don’t work under a contract of employment. Instead, they are independent business owners who provide services or goods to clients or companies.

- Self-employed people are responsible for their own tax and National Insurance contributions.

- They will invoice you for any work they do for your business

- If you work in construction, you may provide work to contractors under the CIS scheme. These people are not paid via payroll either, but you may need to make deductions under the CIS scheme.

Temporary or agency workers in the UK are a bit different from both full-time employees and self-employed contractors.

Temporary workers are employed on a short-term basis by an employer. They could be hired to cover for absences, peak periods, or specific projects.

- They are paid through payroll, and income tax and National Insurance contributions are deducted by the employer.

Agency workers are hired through a recruitment agency and typically work for a client business. The agency is their employer, not the business where they work.

- The agency will invoice you for the cost associated with the workers they have provided.

When an agency is based abroad, but you or your business are hiring agency workers in the UK, the situation can become a bit more complex.

Students can be employed as part-time workers, or they can be self-employed.

- If they are employed, they are still entitled to employment rights under UK law.

- If they are self-employed, they are responsible for their own taxes (via Self-Assessment), and they aren’t entitled to the same employment protections as part-time employees (e.g., holiday pay).

Volunteers are not employees. As such, they do not receive a salary or pay, but they may be reimbursed for certain expenses related to their work.

Payroll: Register with HMRC for PAYE

If you are going to be employing people, then the first thing you need to do is register as an employer with HMRC.

Online registration is the fastest and easiest way to register with HMRC.

You can register via the HMRC website.

The process generally takes about 10 minutes, but you’ll need certain information to complete the registration:

- Your business name (if applicable).

- Business address.

- Your contact details (phone number, email).

- The date you started employing people or the date you first intend to pay employees.

- Company registration number (if you’re a limited company).

- VAT number (if applicable).

- The number of employees you expect to have.

- Your business type (for example, sole trader, limited company, partnership).

- Your unique taxpayer reference (UTR) if you’re self-employed or the business is a sole trader.

It can take a few weeks for your PAYE reference numbers to come through.

You can’t register for payroll if you are not intending to employ anyone for at least 2 months

Payroll: Understanding Pay

Starter Checklist & P45

A Starter Checklist is a form used when a new employee begins working for an employer. It helps the employer collect essential information about the new employee, including their tax status, so that PAYE deductions can be calculated correctly. It’s particularly useful for employees who don’t have a P45.

- Personal Information: Full name, address, date of birth, and National Insurance number.

- Previous Employment: The employee must declare whether they were employed in the current tax year (this determines their tax code).

- Student Loan: If applicable, the employee will state whether they are liable for student loan repayments.

A P45 is a formal document given to an employee when they leave a job. It provides details of their earnings and the amount of tax that has already been paid in the current tax year.

Payroll: Minimum Wage

Minimum Wage in the UK (2025-2026)

The National Minimum Wage (NMW) and National Living Wage (NLW) are the legally required minimum hourly pay rates for workers in the UK, based on age and status.

| Age Group | Hourly Rate |

| National Living Wage (NLW) (21 and over) | £12.21 |

| 18-20 years old | £10.00 |

| Under 18 years old | £7.55 |

| Apprentices (under 19 or in first year) | £7.55 |

It’s critical for employers to ensure that individual deductions (like uniform costs) or payments (like a uniform allowance) do not push an employee’s net pay below the required National Minimum Wage (NMW) or National Living Wage (NLW).

Employers must ensure they pay at least the minimum wage; failure to do so can result in penalties from HMRC.

Tips, Gratuities, or Service charges

Workers who receive tips, gratuities, or service charges from customers must have these payments passed on to them. It’s a legal requirement for employers to ensure that all tips are distributed fairly and transparently to workers. This includes all payments made by customers as part of the service provided, whether it’s cash, card payments, or through online platforms

Payroll: Statutory Deductions

| Deductions | Description | How it Works | Rate/Threshold |

| Income Tax (PAYE) | Deduction based on employee’s earnings, after personal allowance. | Automatically deducted via PAYE system based on the employee’s tax code | – Personal Allowance: £12,570 (tax-free) – Basic Rate: 20% – Higher Rate: 40% – Additional Rate: 45% |

| National Insurance (NICs) | Mandatory contribution to state benefits such as pensions and healthcare. | Deducted based on earnings, with different rates for employees and employers. | – 8% on earnings between £242 (£12,570 p.a.) and £967 per week. – 2% on earnings above £967 per week. |

| Employer’s NICs | Employer’s contribution to National Insurance for employees. | Employers pay NICs for employees earning above £175 per week. | 15% on earnings above £96 per week, £5k p.a. |

| Pension Contributions (Auto Enrolment | Contributions made to employee pension schemes. Employers must auto-enrol eligible employees. | Employee and employer both contribute to pension schemes. | The minimum contribution is 8%, with the employer having to pay a min of 3% and the employee making up the difference |

| Student Loan Repayments | Deduction from employee’s salary to repay student loan, based on income. | Deductions made via PAYE if employee earns above repayment threshold. | Depends on the plan type. |

| Apprenticeship Levy | Tax for businesses with annual pay bills over £3 million, to fund apprenticeships. | Employers with annual payrolls over £3 million pay this levy. | 0.5% of the annual pay bill, with a £15,000 allowance. |

| Attachment of Earnings Orders (AEOs) | Deductions from salary to pay court-ordered debts such as child maintenance or fines. | Employers deduct the specified amount and send it directly to the relevant authority. | Varies depending on the court order. |

| Other Deductions (Voluntary) | Deductions for voluntary payments such as union dues or charity contributions. | These are typically based on employee choice and can be deducted at source. | Varies depending on the agreement (e.g., union fees, charitable donations). |

Payroll: Tax Code

The tax code is based on your personal allowance (the amount you can earn before paying tax). For example:

- A tax code of 1257L means your employee can earn £12,570 tax-free.

- If income exceeds this threshold, income tax will be deducted at the appropriate rate for the income above that amount.

- If the tax code is wrong, your employee may end up paying too much or too little tax.

Common Tax Code Letters

| Amount | Meaning | Used For |

| L | Standard personal allowance (entitlement to £12,570 tax-free) | Most employees without special circumstances |

| M | Marriage Allowance (part of partner’s allowance transferred to you) | Employees receiving Marriage Allowance |

| BR | All income taxed at 20% (basic rate) | Second jobs, pensions, or where no personal allowance is used |

| T | HMRC needs to check your tax situation (unusual circumstances) | Temporary code while HMRC reviews your situation |

| K | Taxable income exceeds personal allowance (additional tax owed) | When income or benefits push income above the allowance |

An employer receives an employee’s tax code directly from HM Revenue and Customs (HMRC). This happens either when the employee starts a new job or when there are changes to their tax situation. HMRC typically sends the tax code through a P9 notice (also called a tax code notice) to the employer, which outlines how much tax-free income the employee is entitled to and which deductions should be applied. Employers are required to use the tax code provided to calculate the correct amount of income tax to deduct from the employee’s pay.

In some cases, employees may also receive a notification from HMRC directly, advising them of their tax code. The employer is legally obligated to apply the tax code provided by HMRC to their payroll system, ensuring the correct amount of tax is deducted. If there are any discrepancies, the employee can contact HMRC to request a review or correction of their tax code.

Payroll: Deductions

For a salary of £15,000 with a tax code of 1257L the employee is entitled to the personal allowance of £12,570 per year, meaning they can earn this amount tax-free. This works out to £1,047.50 per month. With a monthly salary of £1,250, the employee’s taxable income is the difference between their salary and the tax-free portion, which is £1,250 – £1,047.50 = £202.50. This taxable amount is taxed at the basic rate of 20%, resulting in a monthly tax deduction of £40.50. Therefore, the employee’s net monthly pay will be £1,250 – £40.50 = £1,209.50.

| Description | Amount |

| Gross Monthly Salary | £1,250.00 |

| Personal Allowance (monthly) | £1,047.50 |

| Taxable Income | £202.50 |

| Income Tax (20% on taxable income) | £40.50 |

| Pay after Tax | £1,209.50 |

National Insurance Calculation (Employees)

For a salary of £15,000 per year, National Insurance (NI) contributions are calculated separately from income tax and are not influenced by the tax code. In the UK, employees pay Class 1 National Insurance if their earnings exceed the primary threshold of £12,570 per year. For the portion of earnings above this threshold—£15,000 – £12,570 = £2,430—the employee will pay 8% National Insurance, which is the standard rate for earnings between the primary threshold and the upper earnings limit (which is £50,270 for the 2025/26 tax year). Therefore, the total NI contribution for the year would be £2,430 x 8% = £194.40, or £16.20 per month. This amount is deducted alongside income tax but is unrelated to the tax code, as National Insurance contributions are based on earnings and thresholds, not tax allowances.

| Description | Amount |

| Annual Salary | £15,000 |

| Primary Threshold (NI exemption) | £12,570 |

| Earnings Above Threshold | £2,430 |

| National Insurance Rate (8%) | 8% |

| Annual NI Contribution | £2,430 x 8% = £194.40 |

| Monthly NI Contribution | £194.40 ÷ 12 = £16.20 |

Employee National Insurance for Directors who are paid PAYE

Directors of a company can opt for cumulative National Insurance (NI) contributions, which calculates NI based on their total earnings for the tax year rather than each pay period. This method is particularly beneficial for directors who are the only person on the payroll, as it often means that deductions only have to be paid over to HMRC at the back end of the tax year, depending on the Director’s level of earnings. To use cumulative NI, the director must make the necessary adjustments in the payroll system.

Employers National Insurance (ERS)

Employers must pay National Insurance contributions (NICs) on employee earnings above £5,000 per year at a rate of 15% from April 2025. NICs are calculated based on salary and paid in proportion to the pay period. Employers can reduce their NICs liability by claiming an Employment Allowance, which provides up to £10,500 annually from April 2025. However, only one company in a group or connected businesses can claim the allowance.

This is a tax-deductible expense for the business.

Pensions

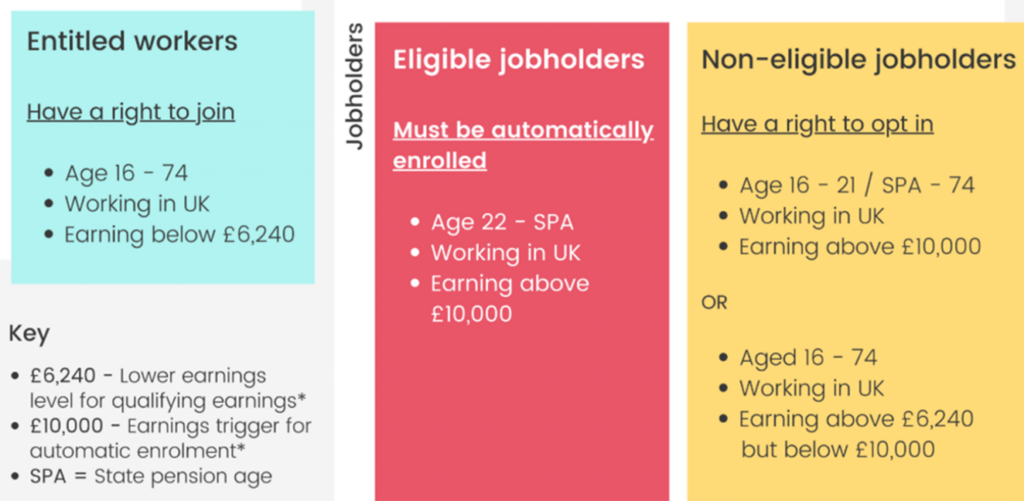

Automatic enrolment became a legal requirement in 2008 in the Pensions Act 2008. It ensures employees over 22, earning above a certain threshold, are automatically enrolled in a workplace pension when they start a job. Employers must:

- Choose a pension scheme that meets the legal requirements for automatic enrolment

- Assess employees eligibility each pay period, based on the criteria in the table below

- Automatically enrol Eligible Jobholders

- Notify employees of their pension status, including any changes or postponements

- Process opt-outs (but not discuss opting out with any employees)

- Allow certain employees to voluntarily join the pension scheme and keep them informed about eligibility and contributions

- Make monthly payments to the pension provider (can set up a direct debit)

- Communicate with employees – Send letters informing employees when their status under auto-enrolment rules changes.

- Complete a declaration of compliance with The Pension Regulator, confirming that the automatic enrolment duties have been met, you must do this at the start, and then repeat the process periodically.

By following these rules, employers ensure employees are properly enrolled and aware of their retirement options.

Opting out and re-enrolment

When you enrol an employee into your pension scheme, they will receive an enrolment pack. In it will be details on opting out. You must not discuss opting out with your employees. Everything they need to know will be in the pack, including how to go about opting out, if they choose to. The opt out rate is much lower than was originally anticipated when the regulations came in.

If they opt out within the deadline set (in the pack), both your employee and you get the contribution made in the first pay where you auto-enrolled them, returned.

If an employee opts out, you must re-enrol them every three years, and they must follow the same opt out procedure again

Contributions

The minimum contribution level is 8% of qualifying earnings (between £6,240 and £50,270 p.a. in the 25/26 tax year). As an employer, you must contribute a minimum of 3%, with your employees paying the remainder.

The pension deducted via payroll, plus your employers contribution, must be paid to your pension provider around the 10th of the following month. You can pay by Direct Debit.

This is a tax-deductible expense for the business.

Statutory Sick Pay (SSP)

It is important to note that some big changes to the SSP system and other elements of employing people have been proposed and are likely to come in later in the year, so please check the current rules when applying SSP, as they may have changed from the time of writing this document.

Sick pay policies should be outlined in employees’ contracts and must meet the minimum requirements for Statutory Sick Pay (SSP). To qualify for SSP, employees must be employed (i.e., have worked for the employer), earn an average of at least £125 per week, and be ill for more than three days in a row. SSP is £118.75 per week (pro-rata) for up to 28 weeks, but the first three days of illness are not eligible. Employees can self-certify for the first week of sickness, but after that, a doctor’s note (fit note) is required.

There are specific rules around SSP for part-time workers, pregnant employees, and other circumstances, so it’s important to seek advice if unsure. SSP is paid through payroll, ensuring the correct amount is deducted from the employee’s earnings based on their eligibility.

SSP is not recoverable from the government, but it is a tax-deductible expense.

Statutory Maternity Pay (SMP)

Statutory Maternity Pay (SMP) is available to employees who meet specific criteria: they must provide proof of pregnancy, have been on the payroll for 26 weeks up to the qualifying week (the 15th week before the expected week of childbirth), earn at least £125 per week, and be on the payroll in the qualifying week. SMP is paid as 90% of the employee’s average weekly earnings before tax for the first 6 weeks, and then either £187.18 or 90% of their weekly earnings (whichever is lower) for the next 33 weeks. Tax and NI are deducted from these payments.

Employers can reclaim 92% of SMP paid, or 103% if they qualify for Small Employer’s Relief (if their NI payments were less than £45k in the previous year). The reclaim process is done via payroll.

Payslips

In the UK, employers are legally required to provide payslips to their employees and workers, including those on zero-hours contracts and agency workers. Payslips must be issued on or before each payday, whether that is weekly, bi-weekly, monthly, or another frequency determined by the employer

Payslips can be provided in either a paper or electronic format, ensuring they are accessible to the employee. Most payroll software now produce payslips that are accessible by employees via an online portal.

Payslips should detail:

- Gross pay (earnings before deductions)

- Deductions (e.g., tax, National Insurance contributions)

- Net pay (earnings after deductions)

- Number of hours worked, if pay varies based on time worked

- Employers must also explain any fixed deductions, such as loan repayments or pension contributions, either on the payslip or in a separate written statement provided before the first payslip.

Human Resources (HR)

It is important to note that some big changes to elements of employing people have been proposed and are likely to come in later in the year, so please check the current rules and look out for changes as they come in. If you are ever unsure about any aspect of employment law, speak to your HR advisor.

HR – Employment Contracts

You must provide a written statement of employment particulars within two months of the employee’s start date. This is not technically a full employment contract but serves as a minimum requirement outlining key terms and conditions.

Employment Contract: While not strictly required for all employees, having a formal written employment contract is strongly recommended as it clearly outlines both the employer’s and the employee’s rights and responsibilities.

- What should be included? The written statement or contract should cover:

- Job title and description

- Starting date and duration of employment (if fixed-term)

- Work hours

- Pay and benefits

- Holidays and sick leave

- Notice periods

- Any disciplinary and grievance procedures

- Place of work

- Other terms like confidentiality, intellectual property, or non-compete clauses, depending on the role.

- Why is it important?

- A written contract or statement provides clarity, sets expectations, and offers legal protection for both parties.

- It helps avoid potential disputes over terms and conditions.

- In case of legal issues, having a well-drafted employment contract can be vital in ensuring both parties’ rights are protected.

Eligibility to work in the UK

You must verify the at the employee has the legal right to work in the UK by requesting and checking specific documents. For example:

- A passport

- Residence card

- Work visa

- Or other necessary documentation – if you are unsure, its best to check as failure to check can lead to penalties of up to £20k per illegal worker

Documents need to be originals, and you should first thoroughly check them and then take copies for your records. Records must be kept for the whole term of their employment plus two years after they leave.

In some cases, you can use an online checking service

Holidays: Statutory Annual Leave

Full time employees have a statutory minimum holiday entitlement of 28 days per year. This includes public holidays. This entitlement is pro-rated for part time or temporary employees.

For zero hours contract workers, holiday entitlement is calculated as 12.07% of the total hours worked.

Employees accrue holiday entitlement while working, and includes during sick leave and maternity leave, providing they meet the eligibility criteria.

The method used for calculating your workers holiday entitlement and rules around your holiday system, booking holidays, carrying holidays over and public holidays, should be included in the contract of employment to avoid any confusion.

You must pay your employees holiday pay of an amount that is at least the same as that employee would normally earn if they were working. If the employees working hours or pay fluctuates, holiday pay should reflect their average earnings over the prior 52 weeks.

Calculating holiday pay

Fixed Salary – For employees who earn a fixed salary, with regular hours, then the calculation is simple.

Take annual pay, and divide by 52 weeks, and then again, divide by 5 working days in a week. This is the daily pay rate for that employee when they are on paid leave.

Note. If you offer compressed hours or have different numbers of hours worked on different days, you may want to calculate and pay holiday pay hourly.

Hourly paid employees – For workers who work irregular hours, you need to calculate their average earnings over a period of a minimum of 12 weeks, but ideally 52 weeks.

It is important to remember, that holidays are to be taken, as they are important to workers health and wellbeing, so there are strict rules around when you can pay holiday pay, for holiday days that have not been taken.

Flexibility

Employees have the right to request flexible working arrangements. Although this is not an automatic guarantee of approval.

Currently you need to have worked for the same employer for at least 26 weeks before making the request. These requests can cover things like balancing work and childcare responsibilities, or adjustments for employees with disabilities. But any workers can apply for:

- Remote working

- Part time hours

- Job sharing

- Flexible hours

- Compressed hours

Requests need to be made in writing, and the employer has 3 months to respond to it. Employers are allowed to refuse on specific grounds, such as:

- Cost

- Detrimental effect on the business

- Inability to recruit

- Negative impact on performance

- Lack of work for the employee to do during the proposed hours

- Not feasible due to structural changes

Employees have a right to appeal a decision if their request is refused.

Rights to unpaid leave

Employers may allow employees to take unpaid leave in certain circumstances, and there are also a few circumstances where it is a statutory right. It is always worth checking, based on the specific circumstances of the request.

- Parents can take up to 18 weeks of unpaid leave for each child under the age of 18 (subject to conditions). Often in one-week blocks and up to a maximum of 4 weeks per year per child.

- Statutory paternity leave is 2 weeks of paid leave, but sometimes requests are made to take additional unpaid paternity leave

- Compassionate leave isn’t a statutory right, but most employees would grant leave where an employee needs time off due to the death or serious illness of a close family member. There is no obligations to pay compassionate leave.

- Significant life events can lead to requests for unpaid leave. Employers are under no obligation to grant this type of leave, but they may, depending on the request and the business needs.

- Study leave, or leave for training or study may be requested. It is at the employers discretion whether to provide this leave or not.

- Jury service – employees are entitled to the time off to serve on a jury, but this is generally provided for by the court system, not the employer

- Religious or cultural reasons – at the employers discretion

HR – Probationary Periods

Also known as trial periods, or introductory periods

- Standard Length: A probationary period typically lasts between 3 to 6 months, but the exact length can vary depending on the employer and the role.

Extension: Employers can choose to extend the probationary period if the employee’s performance or conduct needs further evaluation. However, this must be clearly communicated to the employee and documented.

- Purpose of a Probationary Period: The probationary period is intended for both the employer and the employee to assess the fit between the employee and the job.

- Rights During the Probationary Period: Employees on probation still have legal rights under employment law, including:

- Protection from discrimination (e.g., based on age, race, gender, etc.).

- The right to receive the national minimum wage or national living wage.

- Holiday entitlement (pro-rata for the probationary period).

- Protection from unfair dismissal (after 2 years of continuous employment with the same employer, though the probationary period may be a time to assess whether the employee’s performance warrants permanent status).

- Notice Period: During the probationary period, the notice period for termination of employment is often shorter (e.g., one week instead of a month). This is typically outlined in the employees’ contract.

- Termination During the Probationary Period: Termination rights: Both the employer and employee can terminate the employment during the probationary period, often with a short notice period (e.g., 1 week).

- Reason for Termination: If the employer decides to terminate the employee’s contract during probation, they are not required to provide as much justification as they would after the probationary period, but they must still ensure they do not act in a discriminatory manner.

- Dismissal Protections: Employees have protection from dismissal for unlawful reasons (e.g., discrimination, whistleblowing), even during the probationary period. However, they are not entitled to claim unfair dismissal unless they have been employed for at least 2 years.

- Review and Feedback: At the end of the probationary period, the employer typically holds a review meeting with the employee to discuss:

- The employee’s performance, strengths, and areas for improvement.

- Whether the employee’s employment will continue beyond the probationary period.

- The employer can decide to:

- Confirm the employee’s employment on a permanent basis.

- Extend the probationary period if further time is needed to assess the employee’s performance.

- Terminate the contract if the employee’s performance is deemed unsatisfactory.

- Probationary Period in Employment Contract: A probationary period should ideally be outlined in the employee’s contract of employment. The contract should specify:

- The duration of the probationary period.

- The conditions for successfully completing probation.

- The notice period required during probation.

- Any review process or performance expectations.

- It is important for both parties (employer and employee) to be clear on the terms of probation, including what happens if the probationary period is not completed successfully.

Working Time Directive

Whilst this is European legislation, it was incorporated into UK Lax through the Working Time Regulations 1998, and this remains in place.

- The maximum number of hours in a working week – 48 hours (rules apply)

- Rest breaks – workers are entitled to rest breaks. Although these do not have to be paid breaks:

- 20 mins rest break if they work more than 6 hours in a day

- 11 hours rest between working days

- At least 1 day off per week

- Holiday entitlements – covered above

- Night Workers

- Work related health and safety

You must keep records of employees working hours to ensure to comply with the Working Time Regulations

Insurances

You must have employers liability insurance if you employ anyone in the UK

This is a tax-deductible expense.

Health and Safety

Another really complex area of legislation in the UK. I would highly recommend employing a health and safety specialist if you are unsure about your responsibilities

In the UK, the duty of care refers to an employer’s legal and ethical obligation to ensure the health, safety, and well-being of their employees while they are at work. This duty is grounded in a range of laws, including the Health and Safety at Work Act 1974, the Employment Rights Act 1996, and other relevant health and safety regulations. Employers have a responsibility to take all reasonable steps to protect their employees from harm.

- Risk Assessment: Employers are required to assess the risks to employees’ health and safety in the workplace and take steps to mitigate those risks. This includes identifying potential hazards (physical, psychological, etc.) and implementing measures to prevent accidents or injuries.

- Workplace Safety: Employers must provide a safe working environment, which includes safe equipment, appropriate lighting, ventilation, fire safety, and ensuring that employees are not exposed to harmful substances or dangerous working conditions. Depending on the workplace and the number of employees, you may need to provide trained first aiders.

- Training and Information: Employers must provide employees with the necessary training and information to work safely. This includes induction training, ongoing safety training, and clear instructions on how to handle equipment or substances safely.

- Mental and Emotional Well-being: The duty of care extends beyond just physical safety. Employers must take steps to ensure the mental and emotional health of their employees. This includes preventing work-related stress, managing workloads, and addressing issues like bullying, harassment, or discrimination.

- Providing Adequate Equipment and Tools: Employers must ensure that the equipment provided to employees is fit for purpose, maintained, and safe to use. They must also ensure that employees know how to use this equipment properly to avoid accidents or injuries.

- Reasonable Adjustments for Disabled Employees: Under the Equality Act 2010, employers have a duty to make reasonable adjustments for employees with disabilities. This includes altering working conditions or providing special equipment to help the employee perform their role safely and effectively. This may involve changing working hours, adapting the workplace, or providing additional support.

- Monitoring and Supervision: Employers are responsible for ensuring that employees are not exposed to any unnecessary risks while carrying out their work. This may include regular monitoring of the workplace and providing appropriate supervision to ensure safe practices are being followed.

- Prevention of Workplace Harassment and Bullying: Employers have a duty to prevent and address any instances of harassment, bullying, or discrimination in the workplace. They must establish clear policies on these issues and ensure that there are proper channels for employees to report concerns. Employers should take immediate action when harassment or bullying is reported, ensuring that the workplace remains free of any form of discriminatory or hostile behavior.

- Protection from Dangerous Working Conditions: Employers must provide appropriate measures to protect employees from dangerous working conditions. This could include protecting employees from exposure to hazardous materials, ensuring safe working practices in dangerous environments (e.g., construction sites or factories), and ensuring the workplace is free from physical hazards like slips, trips, and falls.

- Protection Against Discrimination: Employers must ensure that employees are not discriminated against or subjected to unfair treatment based on protected characteristics under the Equality Act 2010 (e.g., gender, race, disability, religion, or sexual orientation). This is part of the employer’s duty of care to provide a fair and inclusive working environment. The duty also extends to ensuring that employees are not harassed or bullied because of their protected characteristics.

Disputes between employers and employees

In the UK, disputes between employers and employees can arise for a variety of reasons, including disagreements over pay, working conditions, performance, dismissal, discrimination, or disciplinary actions. The law provides clear processes for addressing these disputes, and it’s important for both employers and employees to follow proper procedures to resolve issues effectively.

I would highly recommend seeking specific advice from a professional in this field if you find yourself in a dispute situation as the tribunal process is both time consuming and expensive.

Autumn Budget 2025 – How will it impact your business?

The Autumn Budget, announced on 26 November 2025, introduced a range of changes that business owners need to be aware of. From updates to taxation and compliance rules, to adjustments in incentives and support schemes.

Risk and Resilience in Your Business

Running a business can be risky. There are so many things that can impact your performance, and profit. Potentially destroying all that you worked so hard to build. Some of these things are impossible to plan for, but lots of potential risks can be mitigated by identification and planning.

Business Basics – Cash Flow v Profit

Many small business owners can get confused when looking at numbers relating to their business, and often this is due to cash and profit being understood as one and the same thing. It is crucial to understand the difference between these two metrics so that decision making is not flawed.

Business Basics – Project Evaluation

Projects can be anything from taking on a new person, or launching a new product, to building a manufacturing site, or acquiring a business to merge with the current one. How you evaluate each project can vary depending on size and complexity. But undertaking the exercise leads to better decision making and control.

Building Resilience and Sustainability into your Farming Business

Resilience and sustainability lie at the heart of modern farm business strategies, ensuring that agricultural enterprises can withstand economic shocks, adapt to evolving environmental regulations, and maintain profitability amid climate volatility. By embedding sustainable practices, ranging from energy efficiency to regenerative soil management, farmers not only safeguard their livelihoods but also contribute to broader goals of food security and environmental stewardship.

Business Basics – Shared Ownership

Directors and shareholders of UK companies have many rights and responsibilities, but how do these change when you are one of a number of shareholders in a company?

Business Basics – Selling a Business or Shares in a Business

Being aware of your business's value enables you to determine a fair selling price for some or all of your shares and negotiate efficiently with prospective buyers. But where do you find a buyer for your shares, and what happens now?

Business Basics – How much is your Business Worth

Being aware of your business's value enables you to determine a fair selling price for some or all of your shares, negotiate efficiently with prospective buyers, and secure beneficial financing deals, among other advantages.

Business Basics - Forecasting

Although we don’t have a crystal ball, so forecasts are fundamentally informed guesses, businesses need to use them to make informed business decisions and develop business strategies.

Business Basics – Accessing Capital for Growth

Gaining access to outside investment means you don’t have to give up on your dream. So how do you prove to any potential investor that your business model is worth

Farm Diversification: Where to start

According to DEFRA, 71% of farm businesses in 2023/24 have some form of diversified activity, up from 61% in 2014/15. Income from these activities produced £1.393 billion in 23/24, up from £1.321 in the previous year. This demonstrates how important these income streams have become.

Business Basics – Making Tax Digital

Making Tax Digital (MTD) for Income Tax and Rental Income is the biggest change to Self-Assessment since it was launched by HMRC over 30 years ago.

Young Entrepreneur Guide

Do you have a business idea? Or do you want to work for yourself? Then the Young Entrepreneur Guide is here to help you!